A publication examining the issues for our clients

Whats in this issue;

- “JRx” Rebrands to “PP Rx”

- EMA Now Includes Payroll Capability

- New Guild Gov. Pharmacy Agreement

- The Team Helping You Take Care of Business

A word from the editor

By Mark Nicholson “JRx” Rebrands to “PP Rx”

For over five years now JR Pharmacy has been part of the Pitcher Partners network and together with our clients have been able to utilise the expanded resources that attach to a national network – i.e. systems, staff training, website management, superannuation and wealth management advisory, audit and forensic skills etc – while also being able to maintain our heritage “JR” brand. Recently however it has become evident that the Pitcher Partners and JR names have become interchangeable for the majority of our clients as well as many others within the Pharmacy Industry.

Given this high level of awareness, and our preference to simplify our branding, we are pleased to announce that from July 1, JR Pharmacy will change name and commence trading as “Pitcher Pharmacy”. This will align our Pharmacy division with the remainder of our Brisbane Practice which changed its name from Johnston Rorke to Pitcher Partners in 2012. Please note that there will be no other fundamental changes to our business – i.e. we will continue to operate as the same partnership with the same ownership and staff from the same premises.

New Guild Government Pharmacy Agreement

After much negotiation, the new Guild Government Agreement has now been signed with key announced features including a significant increase in services funding, replacement of mark-ups with fixed handling fees, reduction in application of the premium free incentive, ability to discount the co-payment and a review of location rules to occur within the first two years of the Agreement.

On balance and despite the expected negative impact from the copayment discounting option, we consider the Agreement to be a positive outcome for Pharmacy owners, employees, patients and financiers. In many ways however nothing has changed, i.e. the main challenge for all Pharmacy businesses remains is how to increase relevance to customers with the

ultimate proof being growth in customer numbers and average retail sale

per customer.

In his column Norman focuses on the financial analysis of the Agreement changes and how to address the reality of ongoing reductions in gross profit per script by enhancing the Pharmacy’s relevance to customers.

EMA Now Includes Payroll Capability

Our EMA (external management accounting) service now includes the ability to outsource your payroll activities as well as the bookkeeping, BAS and management reporting functions. Annette explains further in her column.

Enjoy this edition and should you have any queries please call myself, Norman or Teresa.

External Management Accounting (JR – EMA) system links with PaysOnline

By Annette Ivory-Barker

JR Pharmacy’s all-encompassing External Management Accounting (EMA) System continues to offer our clients a single solution that connects, simplifies and advances existing business systems – all while streamlining costs – in a period where achieving business and profit growth is generally viewed as becoming more difficult.

Enabled by technology and delivered by specialists, our EMA solution has seen a growing number of both existing and new clients connect to the service during the last 12 months.

With structures ranging from single entities to larger, multi-pharmacy groups, our EMA team has been delighted to be able to help reduce paper and processing while providing the industry’s best Pharmacy business reporting and benchmarking package. To further our promise to help clients both improve processes and manage costs, we are pleased to announce that we are now partnering with PaysOnline to offer EMA clients an online payroll processing service.

PaysOnline has been providing a one stop payroll processing service since 1995, specifically aimed at providing small to large businesses with a simple method of payment of salaries and wages to staff.

In an ever increasing environment of changing government legislation, our unique interfaces and easy to use employee timesheets allows for accurate data capturing of employees hours and detailed cost analysis, budgeting and planning; your payroll records and dissection should provide you without fuss, the most accurate and comprehensive records

available to help run your organisation.

When partnered with the JR Pharmacy EMA Solution, the PaysOnline Managed Payroll Solution provides businesses with a comprehensive fully intergraded payroll, HR, Time and Attendance and Rostering Solution in addition to the existing BAS and back office processing function already provided.

To find out how our EMA solution with PaysOnline can enhance your business administration processes email Annette Ivory-Barker at AIvory-Barker@pitcherpartners.com.au or call us on 1300 662 259 or (07) 3222 8444.

The Agreement and the effect of $1

By Norman Thurecht

The recently announced completion of the 6th Guild/Government Agreement is a very positive announcement for pharmacy owners, customers and staff as it provides increased trading certainty for the next 5 years.

There are still some unknowns specifically in relation to service based programs and income but overall the outcome for pharmacy appears to have been reconciled with the savings already delivered by the industry and the need to create a sustainable model for the future. The concern however is that the option to discount the patient co-payment will act to destabilise the surety to stakeholders provided within the body of other changes.

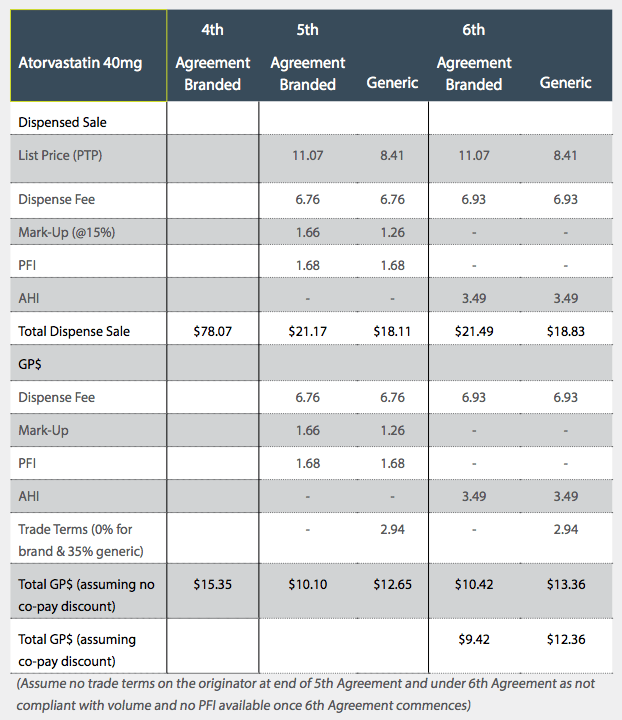

The key change in the 6th Agreement is the replacement of the previous sliding scale markup system with more of a flat “Administration, Handling & Infrastructure” (AHI) fee. The AHI is fixed at $3.49 for items with a list price of less than $180 and increases by 3.5% of the amount over $180 capping out at $70 for items over $2,080.15. The table to the right outlines the difference in sales and GP$ per item dispensed under the new and previous two agreements, for an Atorvastatin 40mg prescription.

Under the 4th Agreement (i.e. pre-price disclosure on this molecule) the net remuneration (and cost to government) was significantly higher than it will be under the 6th Agreement. In addition to the remuneration decrease Pharmacy businesses have incurred significant overhead growth during the same time period causing underlying profit erosion which for a period was hidden and offset by generic trading terms. This is now no longer the case and volume/average sale/professional services income growth will be required to counteract ongoing expenses growth.

In the above example , we have assumed that the brand manufacturer does not provide any trade terms (due to volume non-compliance) however the generic manufacturer provides about 35% discount on the product. The “net into store” price of the generic is therefore reduced to $5.47. Assuming that this is the lowest price the manufacturer can sell the product into pharmacy, then eventually further price disclosure reductions will cause the list price to reduce from $8.41 to somewhere closer to $6. (Note that the price disclosure mechanism means the discounts on high substitution products should settle at <10% otherwise the molecule will be subject to further price reductions). So while the new fee structure uncouples the mark-up from the price reductions, the benefit of trade terms which pharmacies currently receive on branded and generic medicines will continue to decline over time as a result of the ongoing price reductions still impacting manufacturers and wholesalers.

If we overlay the Governments’ proposal to implement one off statutory price cuts to F1 molecules on 1 April 2016 and change to the WADP mechanism to exclude brands with price premiums the erosion of trade terms to pharmacy will be further accelerated.

It has been negatively reported by Pharmacy critics in the media that pharmacies will gain on average $117,000 per annum from the new Agreement compared to the previous one. This raw calculation does not however contemplate volume increases that drive funding increases or remove the cost associated with hospital drugs (eg oncology) which grew considerably throughout the previous Agreement and underpins the majority of cost attached to recent new listings announcements. Equally the critics fail to identify the benefit to taxpayers overall as it actually appears the growth in the 6th agreement spend vs .5th Agreement has been more than offset with price cuts to manufacturers who are potentially the biggest losers from the proposed changes.

Based on our analysis, the new fee arrangement stabilises/improves the margin on dispensing lower cost molecules (i.e. $25 or less) while items costing more suffer a negative outcome. Under the former arrangements we estimated that gross profit dollars per script would bottom out around December 2017 at approximately $10.50 at which point the average sale value per script would be circa $32 and the margin would be circa 33%. It is now likely that the end result in December 2017 will be better (or at least no less than this) however the outcome does depend on the trading terms offered on branded and generic molecules at that time.

Discounting the Co-Payment

As noted earlier, the increased operating certainty offered by the body of changes within the Agreement are negatively impacted by the effect of the ability to commence discounting the patient co-payment by up to $1.00. This is highlighted in the table on page 3, which shows that a decision to discount the co-payment by $1.00 simply decreases the GP$ by $1.00. Therefore, any decision to discount should not be made lightly as the loss of net profit will be significant.

A sample set of client base data (summarised in the table below) supports the results that our average client pharmacy dispensed approximately the same number of scripts in 2012 as they did in 2014. While overall growth was minimal, however, the volume of scripts dispensed within each category changed. For example the general below co-pay increased significantly as a result of the reduction in the value of items dispensed while the largest reduction was in the general category for the same reason.

The concession and entitlement scripts made up 59.2% of the total in 2012 while in 2014 they contributed 61.1% of the total. The growth in this area is a key factor defining the future success of pharmacies because the customers in these categories provide repeat visits and generally have multiple scripts i.e. they are the most profitable customers to have.

Based on the summary sample average, if we assume that a pharmacy dispenses approximately 54,000 scripts (70% of total) where a co-payment is possible, discounting the co-payment by a whole $1 would reduce the gross profit (and resultant net profit) by $54,000 per annum.

In a trading sense, it will directly impact volume, turnover, margins and profitability. But the impact is likely to extend further i.e. as a result of the discounted co-payment, many customers may not reach their safety net threshold which may then change their behaviour in relation to medication usage and prescription filling in future years. Overlayed onto the broader health system it could convert to increased downstream pressure on the Governments’s hospital and Medicare spend.

Therefore, owners need to make a long term considered decision about how to manage customers should they choose not to (or only partially) discount the co-payment. As an example – it may be possible to shift price focus by managing the health of a customer for a fixed monthly payment which equates to the payment of the safety net contribution spread over 12 equal monthly payments. The discussion and conversion will take time and therefore has an imbedded labour cost in it, but the conversation and solution could be broad and valuable enough to eliminate price focussed behaviour.

The Guild and Government have delivered an Agreement that appears to provide a stable platform from which Pharmacy can operate for at least the next 5 years. This platform however can be undermined by the simple decision many owners will likely make to simply discount the “dollar” of patient co-payment. This decision is potentially aided by interest rates being at historical lows but Pharmacy should be aware that ongoing reduction in trading terms is unlikely to be offset by script volume growth. As such debt reduction and business evolution will remain a key feature of those who improve their financial performance throughout the period of 6CPA.

Mark Nicholson

Managing Partner

+61 7 3222 8434

mnicholson@pitcherpartners.com.au

Norman Thurecht

Partner

+61 7 3222 8316

nthurecht@pitcherpartners.com.au

Annette Ivory-Barker

Manager

+61 7 3222 8451

aivory-barker@pitcherpartners.com.au

Teresa Hooper

Partner

+61 7 3222 8461

thooper@pitcherpartners.com.au

Bruce Annabel

Consultant

+61 7 3222 8401

bannabel@pitcherpartners.com.au

Felicity Crimston

Manager

+61 7 3222 8466

fcrimston@pitcherpartners.com.au

Pitcher Partners is an association of independent firms. Liability limited by a scheme approved under Professional Standards Legislation. In Queensland, Pitcher Partners refers to the Queensland partnership and its associated entities.