The last few months have seen improved cashflow in the pharmacy as a result of the improved remuneration in the dispensary – thanks to the higher dispense fees including the AHI fee.

The effect of price reductions flowing through manufacturers and wholesalers will continue to have downward pressure on trade terms in the latter half of this financial year and over the course of the 6th Agreement.

Therefore we believe that this financial year will in effect be a year of two halves. The first half profitability will be up from the previous financial year results but the second half of the year will see some decline as the price reductions of 1 October 2015 and 1 April 2016 begin to takes effect through the whole supply chain.

Suppliers feel this through pharmacy in the form of delayed payments for accounts. Pharmacy feels it because the bank debt requirements do not go away (generally fixed repayment schedules) while trying to balance stock quantities, sales (converting the stock to cash) and the payment of the supplier accounts.

The bank never gets forgotten in this equation because they are fixed and secured. Other suppliers feel the pain. The cycle of juggling payments can carry on for several years because as long as the bank commitments are being made the other suppliers will generally try and negotiate other outcomes to get their account paid.

So the question must be asked why does this happen?

The cashflow issue of dealing with suppliers and banks alike can often feel like it happens suddenly. However the issue actually starts when you purchase or refinance the pharmacy.

What we are seeing in the market today is pharmacies transacting at a value based on an estimate of future maintainable earnings. Borrowings are being sought based on these values (with LVR’s continuing to be at or greater than 70% when the loan is initially set up). However if these estimated future maintainable earnings are not achievable (for many and varied reasons), the cashflow cannot support the valuation previously set and by default the pharmacy cashflow will not be able to support a level of debt.

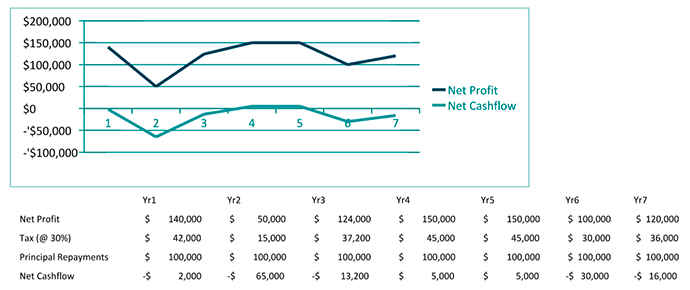

In fact understanding the cashflow impact is the most important concept an accountant can work with you on. As highlighted in the table below, even profitable years can have a negative cashflow because of tax and debt requirements.

There are of course many opportunities to change/improve the pharmacy to lift cashflow but in some respects, as was witnessed in the 2015 financial year, the downward pressure on cashflow caused by PBS price reductions is so great that many pharmacies could not replace the losses faster enough. If you add to that the possible impacts of discounting the co-payment by $1 from 1 January, you must understand the impact on cashflow in the latter part of this financial year.

Therefore the considerations are as follows:

- Understand that the valuation of the pharmacy is inextricably linked to the cashflow;

- What can the cashflow afford as the correct debt level now and into the future;

- How well can that debt level be managed should changes occur – sensitivity analysis;

- How can the business be grown/improved to positively influence cashflow;

- Are there sufficient other cash or assets that can create a buffer should debt reduction be required in a short period of time to get the debt to a manageable position relative to cashflow?

Understanding these considerations before you borrow the money will avoid issues later should the future maintainable earnings of the pharmacy be impacted by issues beyond your control.